Beyond the Mag 7: A Broader Lens on Growth

Long-Term Growth Is All About Earnings

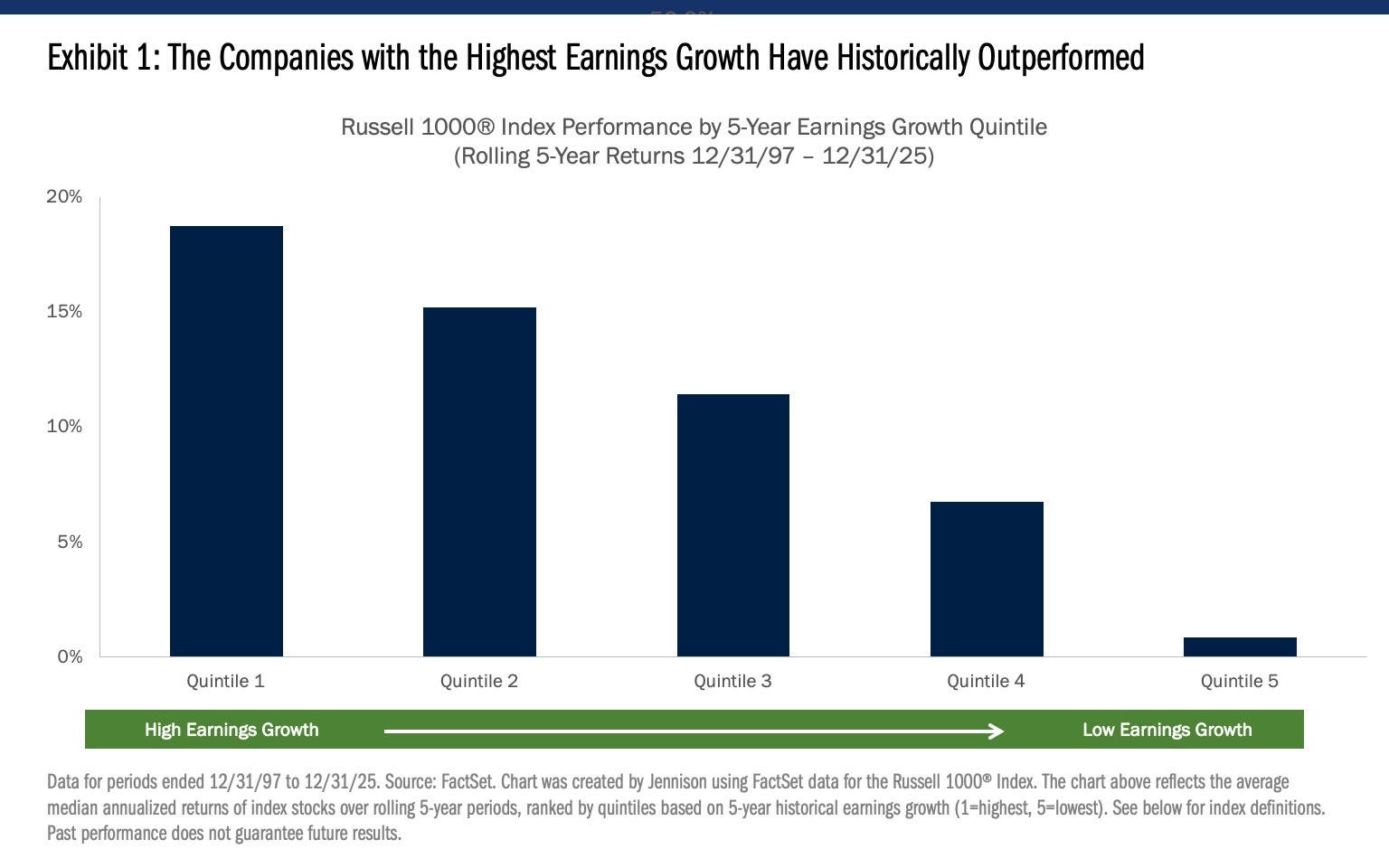

Over nearly three decades, data demonstrating the relationship between company fundamentals and share price returns is unambiguous: the companies with the fastest earnings growth in the Russell 1000 Index have delivered the strongest performance consistently over multi-year time periods (Exhibit 1).

Looking at rolling five-year returns of the Russell 1000 Index from 1997 through 2025, the top earnings-growth quintile produced annualized returns near 19%, compared with less than 1% for the slowest-growing quintile. Over time, investors have clearly rewarded businesses that can compound profit growth at a high and durable rate.

The Concentration Problem

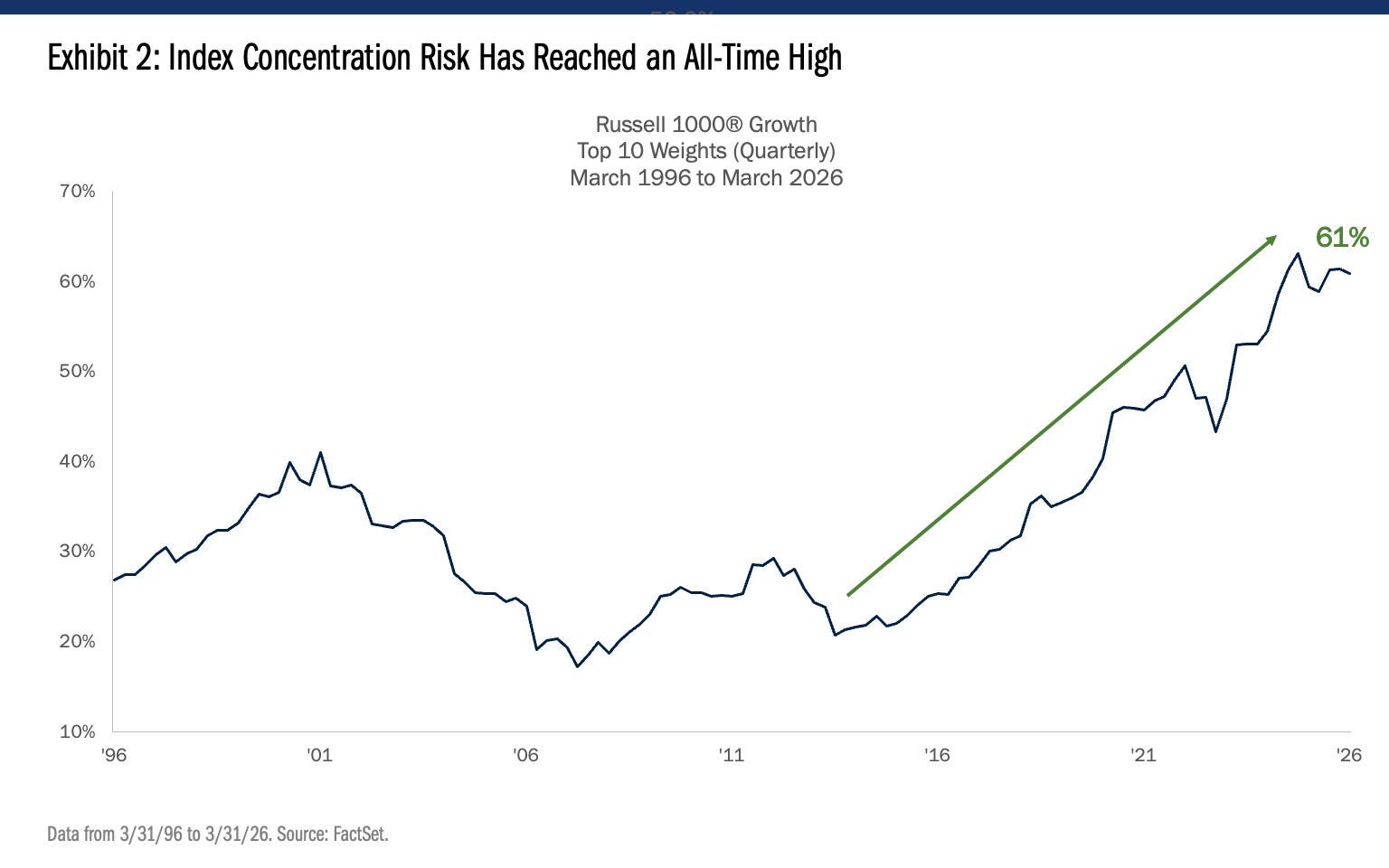

If the long-term case for growth investing is straightforward, the case for accessing it through a passive growth benchmark has quietly become more complicated. The top 10 holdings in the Russell 1000 Growth Index now account for 61% of the index — more than double their average weight over the past three decades (Exhibit 2).

For most of the index’s history, top 10 weights oscillated between 20% and 35%. The current level is without precedent, and it was reached in a remarkably short window: top 10 weights have nearly doubled since 2013, driven by a handful of mega-cap names whose market values have grown faster than the rest of the universe combined.

As a result, a benchmark that was historically a broad expression of secular growth has become, in practice, a concentrated wager on a few of the world’s largest businesses.

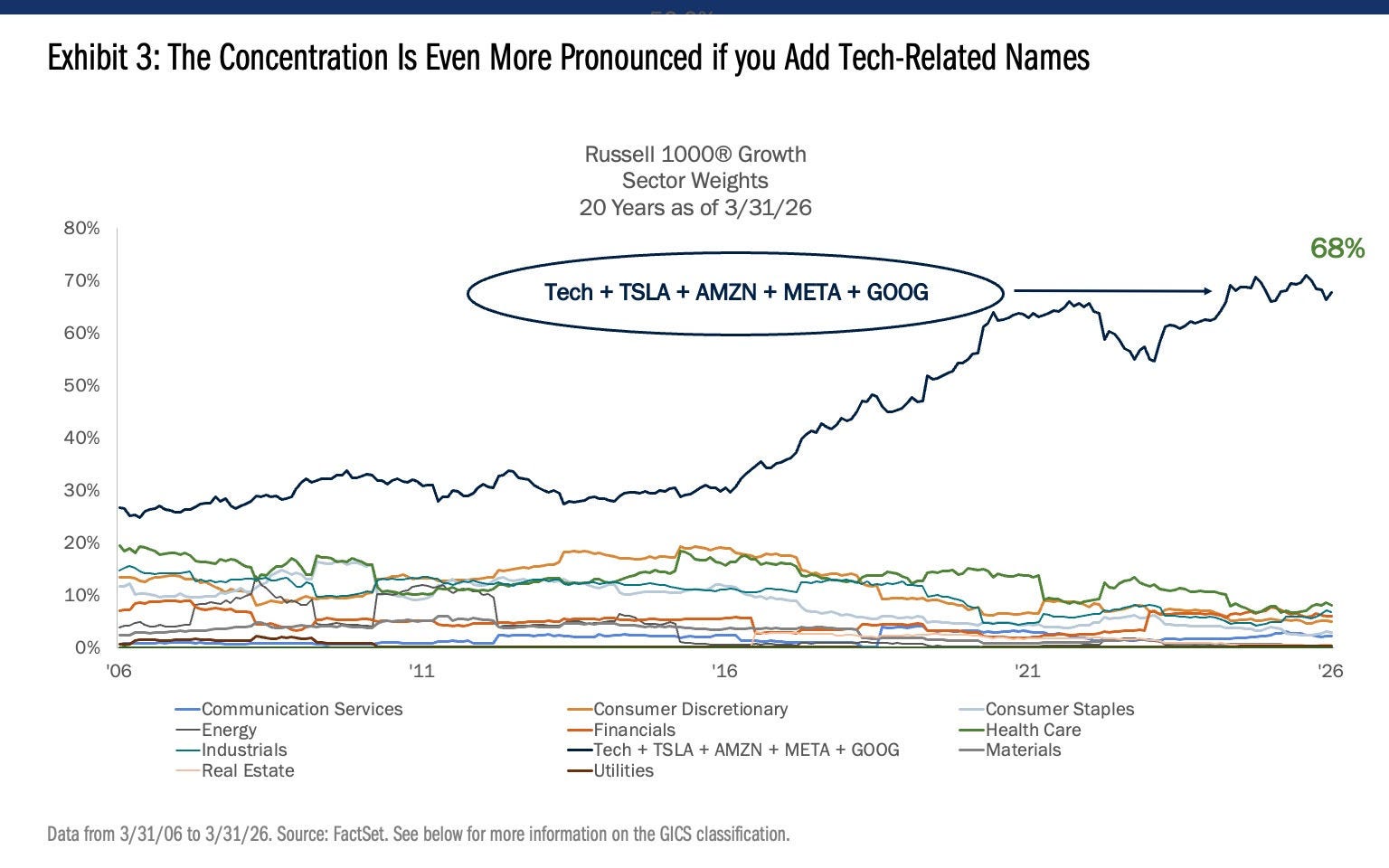

In addition to being heavily concentrated in just a handful of individual stocks, 50% of the Russell 1000 Growth Index is in the technology sector. And when you add tech-related names from other sectors, that number soars to 68% (Exhibit 3).

The Mag 7 Growth Deceleration

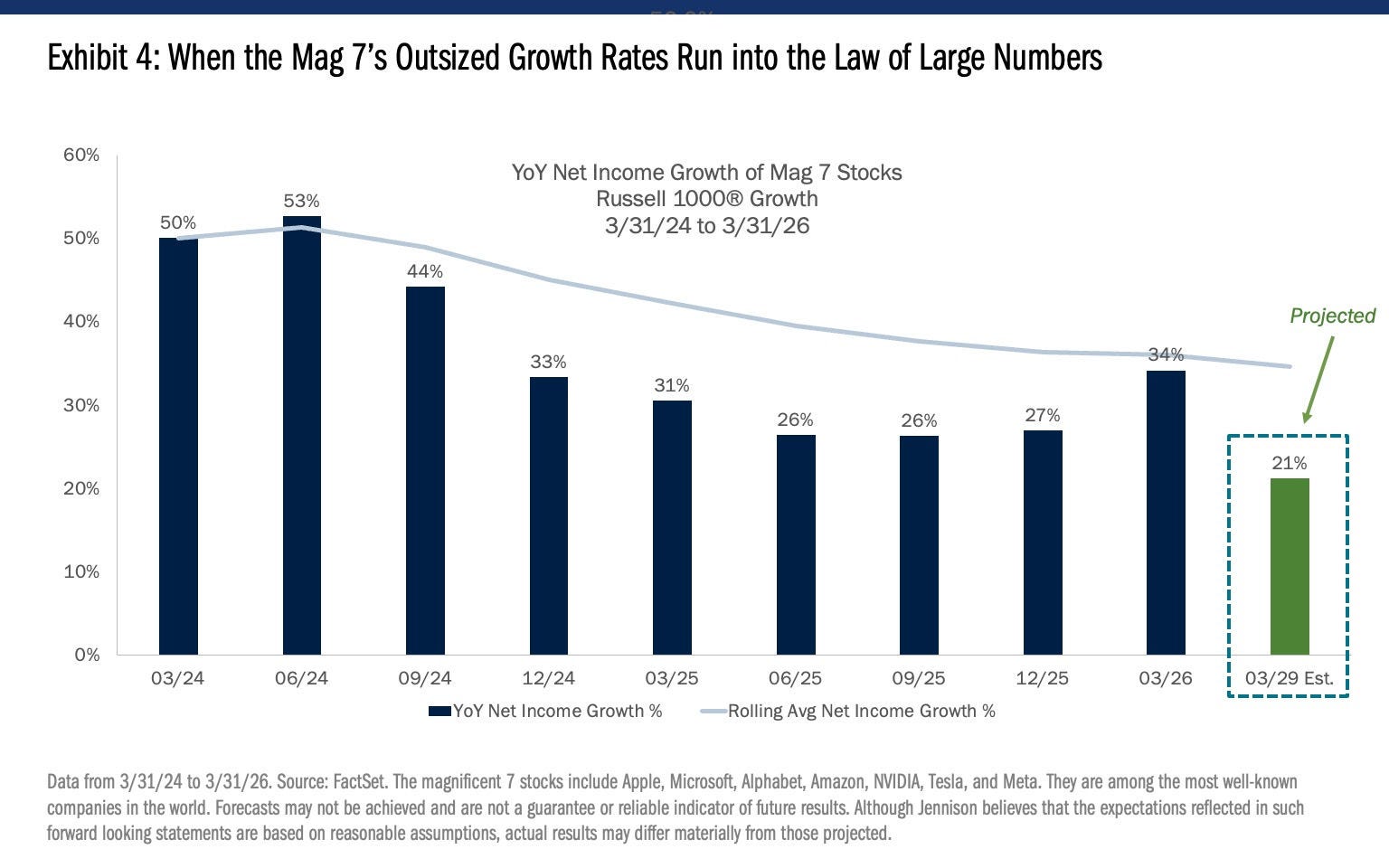

While the Magnificent 7 have been among the fastest growers for years, the reality today is that the cohort’s growth rate has been slowing. They are no longer among the top quintile of growers in the Russell 1000.

Year-over-year net income growth for the Mag 7 peaked at 53% in the second quarter of 2024. By the end of 1Q26, that figure had decelerated to 34%, and consensus projections put it closer to 21% by 2029 (Exhibit 4). The law of large numbers is doing what it usually does to dominant incumbents: making the next double harder than the last. These companies are on a path of normalization toward a still-attractive but no-longer-exceptional growth rate. The companies that were the index’s growth engine are now poised to grow roughly in line with, rather than well ahead of, a long list of less dominant peers.

None of this is a critique of the Magnificent 7 as businesses. These are high-quality companies with durable competitive advantages, exceptional cash generation, and a leading position in the AI build-out. This is simply what mega-cap scale eventually does to the rate of growth.

Positioning for the Next Generation of Leaders

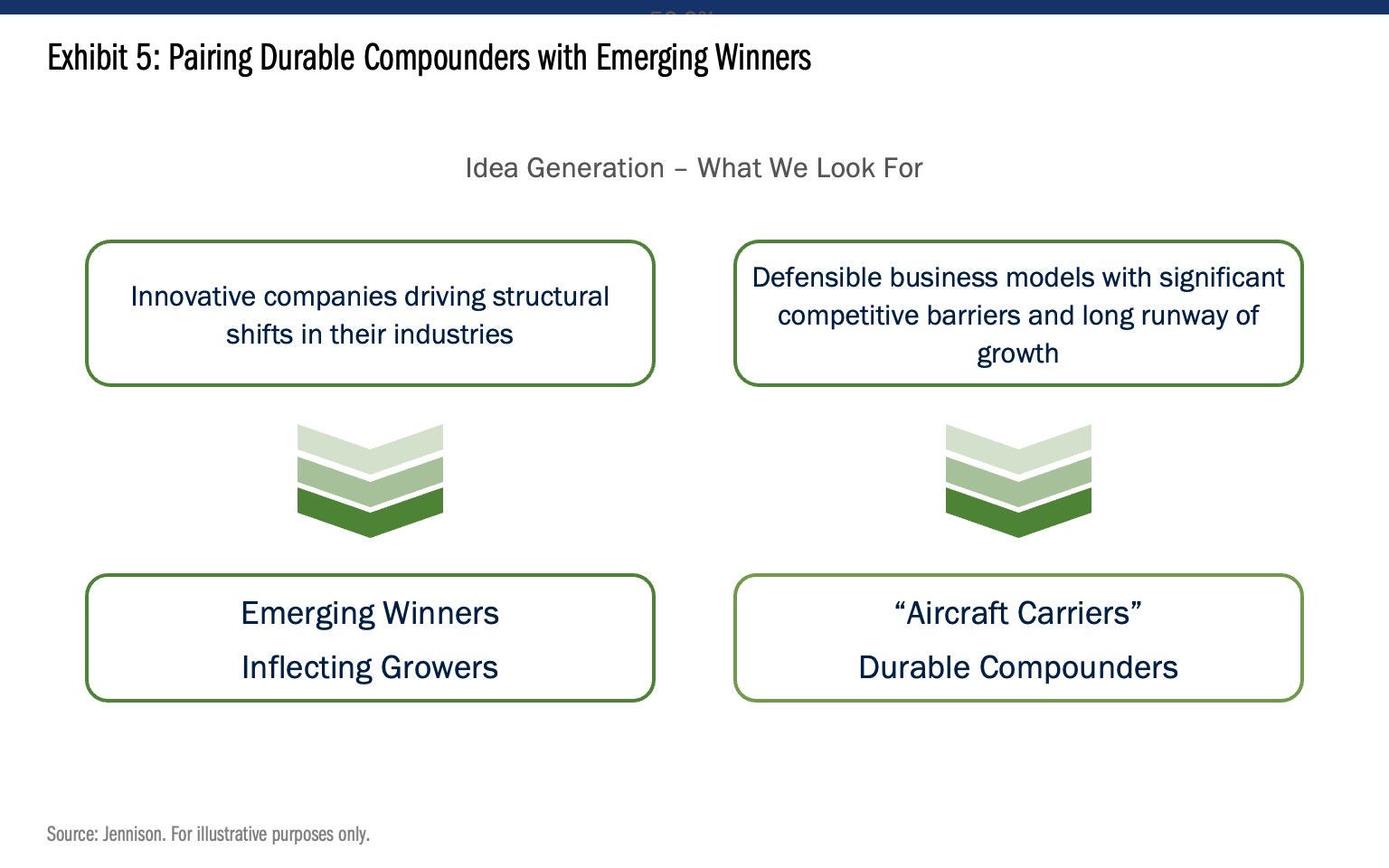

At Jennison, we look for two types of growth companies – those with above-average and potentially accelerating growth and those with more stable and consistent growth (Exhibit 5).

The first are generally the emerging winners in a new and evolving industry or inflecting growers that are innovating within an existing way of doing business. Companies such as these have large and expanding addressable markets and are investing significantly in growth, understating their profits. Many times the market underappreciates the scale of opportunity as they produce earnings that are well below their potential and before the opportunity is fully reflected in benchmark weights. By design, those companies are underrepresented or absent from a top-heavy passive index.

The second are durable compounders — the “aircraft carriers” with defensible business models, significant competitive moats, and long runways of growth ahead of them. These stable growers are high-quality companies, generally with pristine balance sheets, and significant cash flow generation. The market often underestimates the duration of growth of these companies, and the better-than-average returns that their consistent, above-average growth can drive. Many of today’s mega-caps fit this profile.

History shows that market leadership is dynamic: the companies that dominate one era seldom lead the next with the same force. For growth investors, the opportunity is not to abandon proven leaders, but to complement them with emerging winners and inflecting growers that benchmarks may not yet fully recognize. This is where active, diversified growth investing can add meaningful value.

The Russell 1000 Growth benchmark has quietly become a concentrated bet on a handful of mega-cap technology names whose growth is now decelerating. A highly concentrated index means that passive performance becomes dependent on the continued success of a small group of stocks. It does not provide investors with the flexibility to pivot if fundamentals deteriorate or no longer support valuations, nor does it protect from downside risk if leadership changes. In our view, a broader, more diversified growth portfolio gives investors a way to participate in today’s leaders while also owning the businesses most likely to drive the next decade of returns.

Index Definition: The Russell 1000® Growth Index (R1000G) contains those securities in the Russell 1000 Index with a greater-than-average growth orientation. Companies in this index tend to exhibit higher price-to-book and price-to-earnings ratios.

The financial indices referenced herein are provided for informational purposes only. When comparing the performance of a manager to its benchmark(s), please note that the manager's holdings and portfolio characteristics may differ from those of the benchmark(s). Additional factors impacting the performance displayed herein may include portfolio rebalancing, the timing of cash flows, and differences in volatility, none of which impact the performance of the financial indices. Financial indices are unmanaged and assume reinvestment of dividends but do not reflect the impact of fees, applicable taxes or trading costs which may also reduce the returns shown. All indices referenced in this presentation are registered trade names or trademark/service marks of third parties. References to such trade names or trademark/service marks and data is proprietary and confidential and cannot be redistributed without Jennison's prior consent. Investors cannot directly invest in an index.

GICS Classification: The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”) and is licensed for use by Jennison Associates LLC “as is”. As of October 1, 2009, Jennison Associates LLC (“Jennison”) does not reclassify securities classified by S&P/MSCI GICS. Only securities not classified by S&P/MSCI GICS will be classified by Jennison. Therefore, this report may include companies that have been classified by S&P/MSCI GICS or classified by Jennison. Companies classified by Jennison are not sponsored by the S&P/MSCI GICS classification system.